For the past two decades, ASEAN member states have achieved remarkable progress in the energy sector in terms of the acceleration of rural electrification access, rapid provision of large-scale national grid systems, successful mobilisation of indigenous resources, gradual adoption of new technologies and share of renewables into their respective energy mix.

Further, ASEAN is also beginning to see cross-country electricity entry trade bilaterally and power exchanges that will promote the future market of multi-lateral trade.

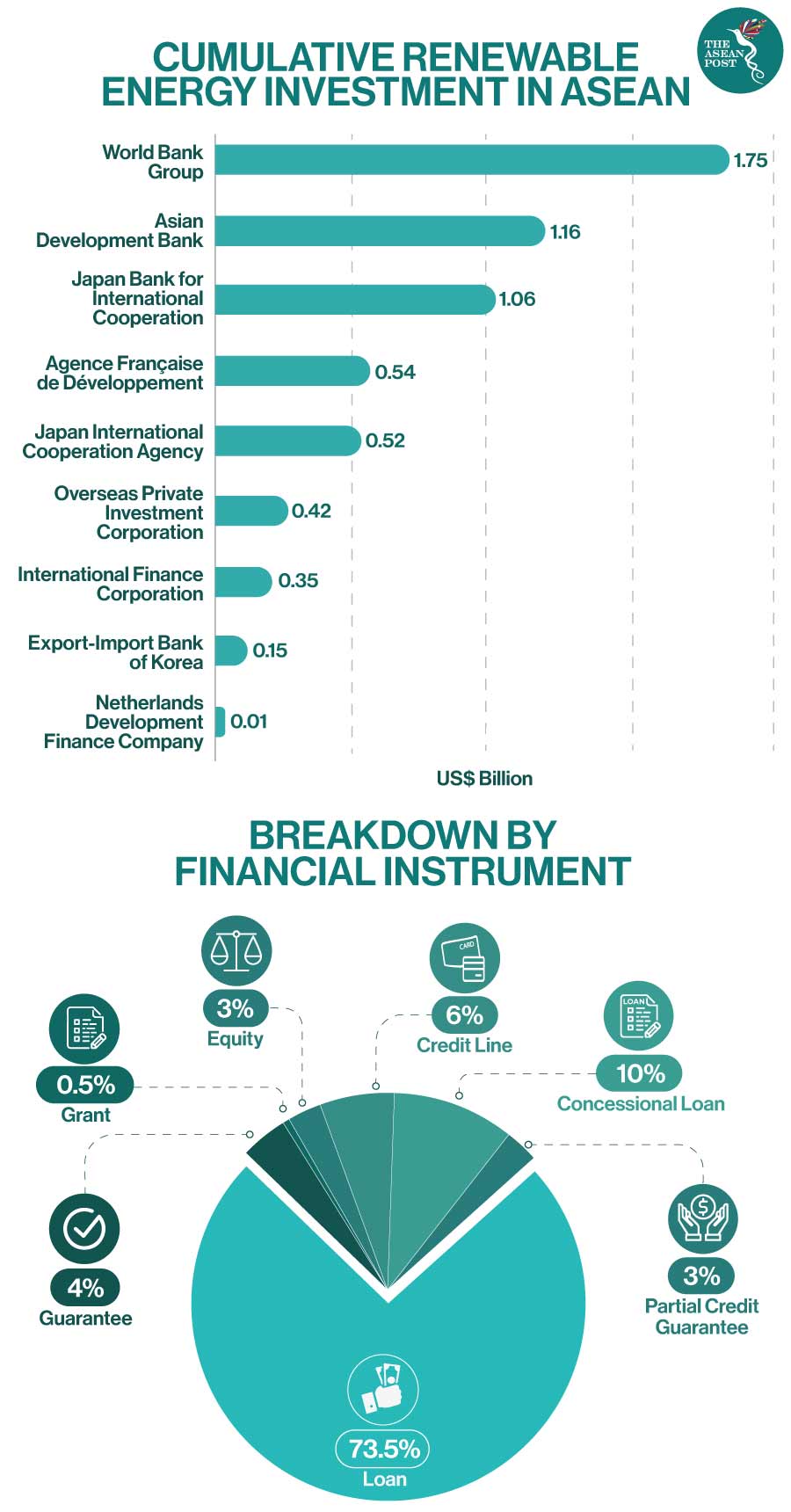

However, the future energy landscape of ASEAN will rely on today’s actions, policies, and investment to change the current dominant fossil fuel-based energy system into a cleaner energy system.

As the world is focused on containing the spread of the COVID-19 virus, policy measures will have mixed outcomes as to when it is appropriate to reopen the economy, either partially or fully, to reduce the economic impact as well as to bring back jobs and ensure strong markets.

What we do know is that the COVID-19 pandemic has already plunged the world’s economy into a recession in which global growth is predicted to contract by -4.9 percent and that of the ASEAN-5 (Singapore, Malaysia, Indonesia, Philippines, and Thailand) by -1.3 percent in 2020.

Global energy demand is expected to fall by six percent in 2020 compared to 2019. However, countries experiencing partial or full lockdown could see energy demand drop by as much as 18-25 percent in 2020. Global oil demand is also expected to decline by eight million barrels per day in 2020.

As a result, global carbon dioxide (CO2) emissions are also expected to fall by eight percent in 2020 compared to 2019 levels.

The crisis has already put 300 million jobs at risk globally, of which 3.2 million out of 40 million in the energy sector may have already been lost. Many millions of jobs in the informal sector have already been impacted severely and millions of people may have already fallen below the poverty line.

During the pandemic crisis, some countries in ASEAN have already faced the challenge of an increasing national debt or depleted national savings as more spending is needed to protect life, wellbeing and the need to have an appropriate stimulus package to save the economy.

Bouncing Back Strongly

Without proper economic stimulus packages, economic recovery will be slow, and the impact will be enormous.

However, when the post COVID-19 era begins, hopefully by 2021, energy demand as well as emissions, are expected to bounce back strongly.

Currently, most of the world including ASEAN member states face tremendous challenges for their future energy landscapes. The energy transition must embrace a new architecture including sound policy and technologies to ensure energy access with affordability, energy security and energy sustainability.

Thus, all decisions and energy policy measures will need to be weighed against potentially higher energy costs, affordability, and energy security risks in a post COVID-19 world.

Given the high share of fossil fuel (80 percent share of oil, coal, and natural gas) in ASEAN’s current energy mix, the clean use of fossil fuel through clean technologies deployment is indispensable for de-carbonising ASEAN’s emissions. Further, natural gas should be promoted as the transitional fuel in ASEAN.

Renewables, energy efficiency, and renewable hydrogen should be accelerated along with the adoption of clean technologies in the medium to long-term. Although they comprise the most abundant energy resources in ASEAN, the ‘intermittent renewables’ solar and wind have so far contributed negligent amounts (2.4 percent in 2020) to the power mix.

Of course, there is a need for reform in the energy sector, especially in the electricity market. There needs to be more open competition in all areas of the electricity market such as generation, transmission, and distribution.

Future Electricity Market

Further reform in rules and procedures will be needed to allow more advanced and competitive technologies to enter the market share of the energy mix rather than using old rules and procedures that favour traditional fuels.

The future electricity market will need to move from the hybrid model ‘single buyer’ to full market competition with an independent power regulator and regional institutional system operator to facilitate wholesale as well as retail markets, and encourage more market players to participate.

In this way, electricity reform will attract foreign investment to modernise the electricity infrastructure including more efficient power systems and the gradual phasing out of inefficient power generation and technologies.

For energy resiliency in a post-COVID-19 world, quality energy infrastructure will need to be promoted and adopted in ASEAN as it will ensure inclusive growth that will bring harmony to people, development, and environment sustainability.

However, ASEAN leaders should take the COVID-19 impact and the period of low oil prices as an opportunity to make serious energy policy reforms such as fossil fuel subsidies.

Developing economies should reach out for international support to ensure that national green economic recovery stimulus packages are sufficient to have long-lasting impact in lowering emissions.

While COVID-19 has delayed many energy-related infrastructure projects, countries need to re-visit their energy policies to ensure that post COVID-19 policies will attract long-term and sustainable investment for clean energy technologies, new sources of clean fuel such as green hydrogen, and renewable energy.

The unbundling of ownership in the electricity market, the non-discriminatory third-party access to transmission and distribution networks, and the gradual removal of subsidies in fossil fuels-based power generation ensure the pre-conditions for market competition by bringing a level playing field to new technologies and renewables entering into the energy mix.

Other necessary policies to attract foreign investment into renewables and clean technologies include fiscal policy incentives (tax holidays), reducing market barriers and regulatory burdens, and policies to reduce upfront investment costs, such as rebated payment systems, through government subsidies and guarantees to make investments more feasible with lower risk.

Related Articles:

Quality Energy Infrastructure For Sustainability

Building Energy Efficiency To Employ ASEAN People