The Association of Southeast Asian Nations (ASEAN) has set an ambitious target of securing 23 percent of its primary energy from renewable sources by 2025 as energy demand in the region is expected to grow by 50 percent. According to the International Renewable Energy Agency (IRENA), this objective entails a “two-and-a-half-fold increase in the modern renewable energy share compared to 2014.”

With the rapidly declining cost of renewable energy generation via such methods as wind and solar photovoltaic (PV), the Southeast Asian region has been presented with a golden opportunity to meet its immense electricity demand in a cost-effective and sustainable manner.

A Southeast Asia Energy Outlook report states that through this, local manufacturing industries will also be able to grow. For example, Malaysia is already the world’s third-largest producer of photovoltaic cells, while investment in Thailand’s solar manufacturing industry is increasing PV output for global markets. By deploying more renewable energy in the region, the economy of these countries can be further strengthened.

Rising energy needs and changing supply-demand dynamics are creating new and tough challenges for Southeast Asia’s policy-makers. Despite existing opportunities created by appropriate policies, some challenges require a region-wide approach.

Key challenges

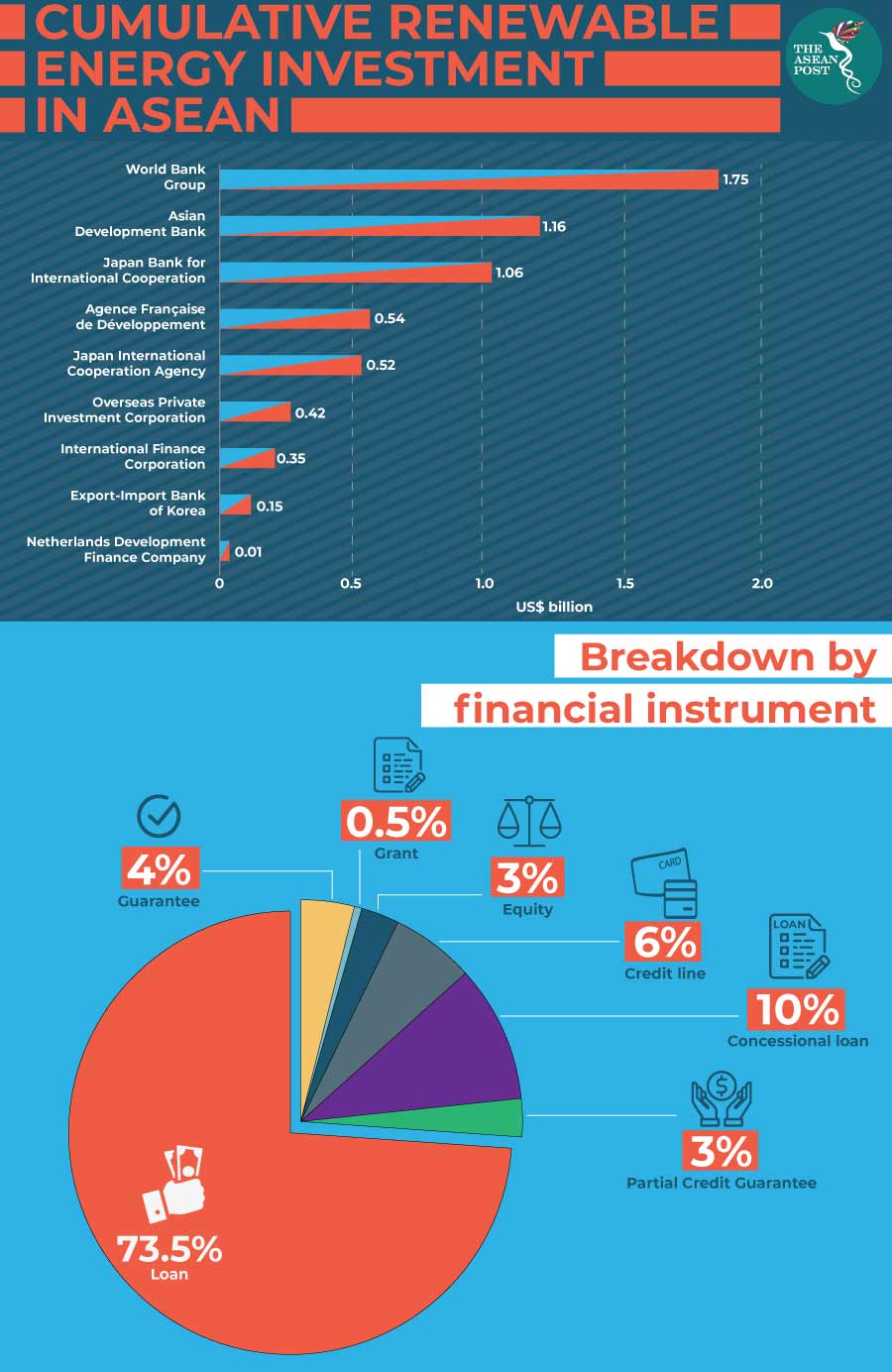

The development of renewable energy projects in the region is an expensive bill for most ASEAN countries to foot. In a brief published by the Habibie Centre, financial access was deemed the most important factor for developing renewable energy projects due to their capital-intensive nature. Currently there is a lack of experience and expertise in some ASEAN member states, particularly in Malaysia, Indonesia, and Vietnam, in evaluating the risk of renewable energy investment.

“To a large extent, the lack of financial support and channels, including the availability of public funding support, has made the renewable energy sector a relatively unattractive sector to invest in,” the brief concluded.

Geographical and technical conditions are some of the challenges faced by renewable energy project developers in the Southeast Asian region. A lack of policies in place to regulate the proper use of land and the subsequent environmental impact is a growing concern when large scale renewable energy projects are carried out in the region.

Specific to Indonesia and the Philippines, is the challenge of limited infrastructure capacity that hinders effective renewable energy deployment, in regard to electricity transmission. This is because both countries are archipelagic in nature, resulting in fragmented electricity grids.

The lack of regulatory framework is another major hurdle when it comes to the introduction and development of renewable energy projects. Brunei, for example, has no specific policy framework in place to regulate the development of renewable energy but is currently studying the possibility of creating one.

Another example would be the lack of coordination amongst government agencies and the private sector as is the case in Lao PDR which effectively hinders the implementation of the country’s renewable energy priorities and policies.

Another obstacle would be the issue of complex bureaucracy as is the case in Indonesia. The State Electricity Company – Perusahaan Listrik Negara (PLN) – monopolises the transmission, distribution and system operation of electricity, and dominates the local electricity generation market which inhibits the interests of potential investors.

Lastly, the lack of awareness and public support also contributes to the challenges faced by ASEAN member states when it comes to developing the renewable energy sector in the region. The minimum use of renewable energy technologies is particularly evident amongst land and building owners and industrial players. This could be due to a lack in awareness about the potential benefits of renewable energy towards environment conservation for a cleaner and greener future.

“The accelerated adoption of renewable energy offers broad environmental, economic and social benefits, including creating jobs, reducing air pollution and tackling climate change,” said IRENA Director-General Adnan Amin.

“Policy makers and other development actors should prioritise investment in clean, reliable and affordable energy as a pillar of development across the region,” he added.

As such, immediate collaboration between the public and private sector is necessary to bridge and meet the challenges at hand. Collaboration in the political and economic domains would work to limit risk perception that might hinder renewable energy investment flows and ensure progress toward achieving the region’s energy goals.

Related articles: