Previously seen as a disruptor to traditional banking methods, blockchain technology is now being adopted by banks in Thailand. In an unprecedented move last week, 14 banks came together and jointly launched the Thailand Blockchain Community Initiative.

Apart from the 14 commercial banks, the Thailand Blockchain Community Initiative will also involve seven corporations and state enterprises. The banks taking part include Thailand’s biggest banks such as Bangkok Bank, Krung Thai Bank, Siam Commercial Bank and Kasikornbank. Meanwhile, the seven corporations and state enterprises who are collaborating on this project include Provincial Electricity Authority, Siam Cement Group and Metropolitan Electricity Authority. They’ve also enlisted the help of IBM to assist with the technology behind blockchain.

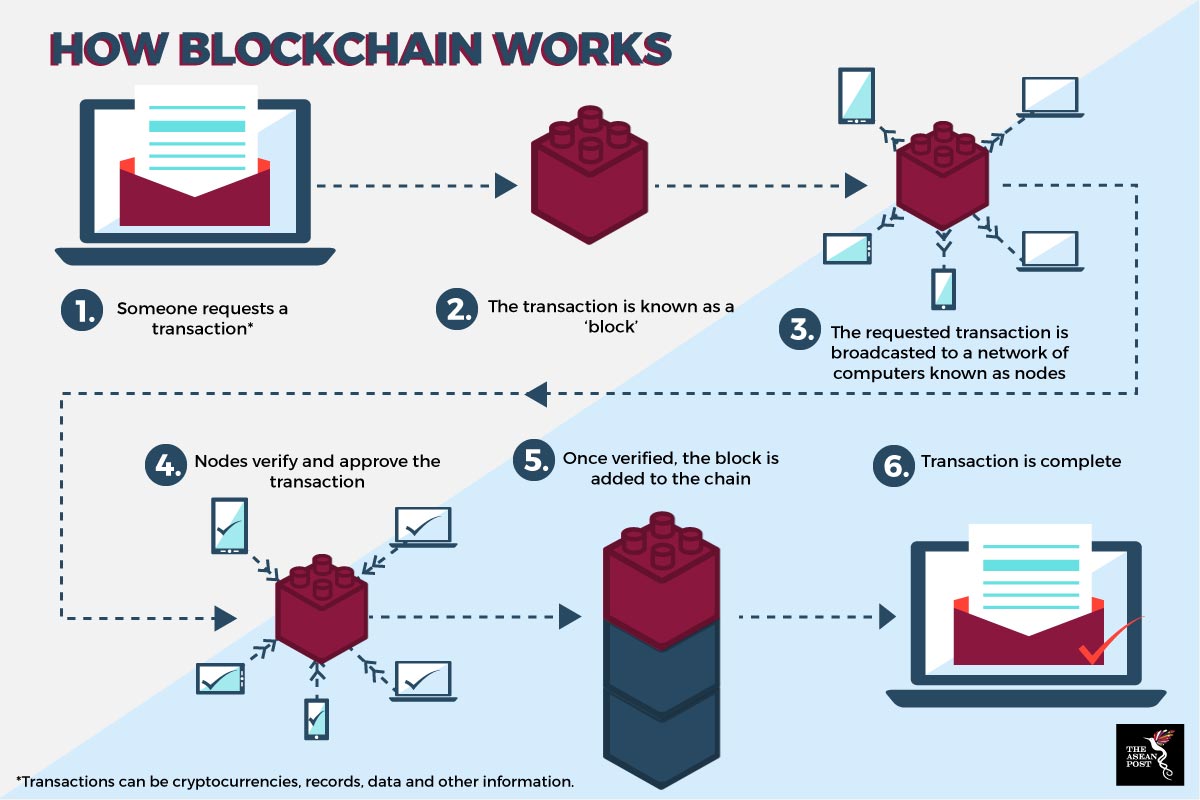

Blockchain – along with cryptocurrency – have become buzzwords recently due to their disruptive nature; challenging traditional notions of finance and banking. Blockchain is essentially a digital ledger consisting of blocks of information that are kept secured by a cryptographic key. Each block is linked to other blocks and for each change that is needed to be made on the ledger, other computers have to verify it first. Before this, blockchain was seen as being disruptive to banks because it eliminates the need for banks to act as an intermediary authority to oversee transactions. However, the Thailand Blockchain Community Initiative sees the potential blockchain has in making banking and finance more convenient.

This initiative will see the 14 banks develop a shared finance platform where they can issue letters of guarantee based on blockchain technology. Letters of guarantee are contracts that banks issue on behalf of a client who has entered into a contract to purchase goods from a supplier and promises to meet any financial obligations to the supplier in the event of a default.

According to Predee Daochai, Chairman of the Thai Banker’s Association, the value of letters of guarantee issued by banks in Thailand in 2017 was worth more than 1.35 billion Thai Baht, an 8% increase from 2016.

The system is currently being tested in the Bank of Thailand’s regulatory sandbox and is expected to be in operation by the third quarter of this year.

One of the major reasons for this initiative is because it is believed that blockchain will help achieve higher efficiency and lower costs. The digitalisation of the letters of guarantee will shorten the process of issuing the letters to as little as half an hour, a stark contrast to the lengthy and bureaucratic process previously which involved much paperwork.

Furthermore, since the platform is shared, banks don’t need to spend money building their own systems and are able to save on cost and streamline an essential financial service.

With integration onto a single platform, banks can ensure the security of their clients and individuals. Since each bank is equally integrated into this initiative, banks would have to do their best to maintain the security of the platform, as a mistake by one bank could damage the entire ecosystem. This system also ensures that banks act as each other’s checks and balances. The security promised by blockchain will also ensure that data is less susceptible to manipulation and can also prevent identity theft.

Despite coming down hard on cryptocurrencies, Thailand has surprisingly embraced blockchain. For example, Siam Commercial Bank is looking to expand its international remittance services through blockchain. Currently, cross-border remittance through blockchain is only available for the Japanese Yen, but due to positive results, Siam Commercial Bank is now planning to add the Euro and Pound Sterling by the end of 2018.

While Thai banks might be embracing blockchain, they still need to be careful with their network architecture and implementation. As with most technologies, there’s always a security risk – even more so when it comes to banks who handle sensitive information and large amounts of money.

The Financial Times recently reported that blockchain still has a long way to go before becoming mainstream in the financial sector. While banks might be slowly integrating blockchain into their processes, the jury is still out on whether blockchain can handle billions of dollars in daily cross-border payments.

By embracing blockchain, Thailand is showing that it is ahead of the curve compared to its Southeast Asian counterparts. If integration of blockchain in its financial services proves to be successful, banks in the rest of the region will surely follow suit.