Having taken the world by storm, green bonds have now reached the shores of Southeast Asia.

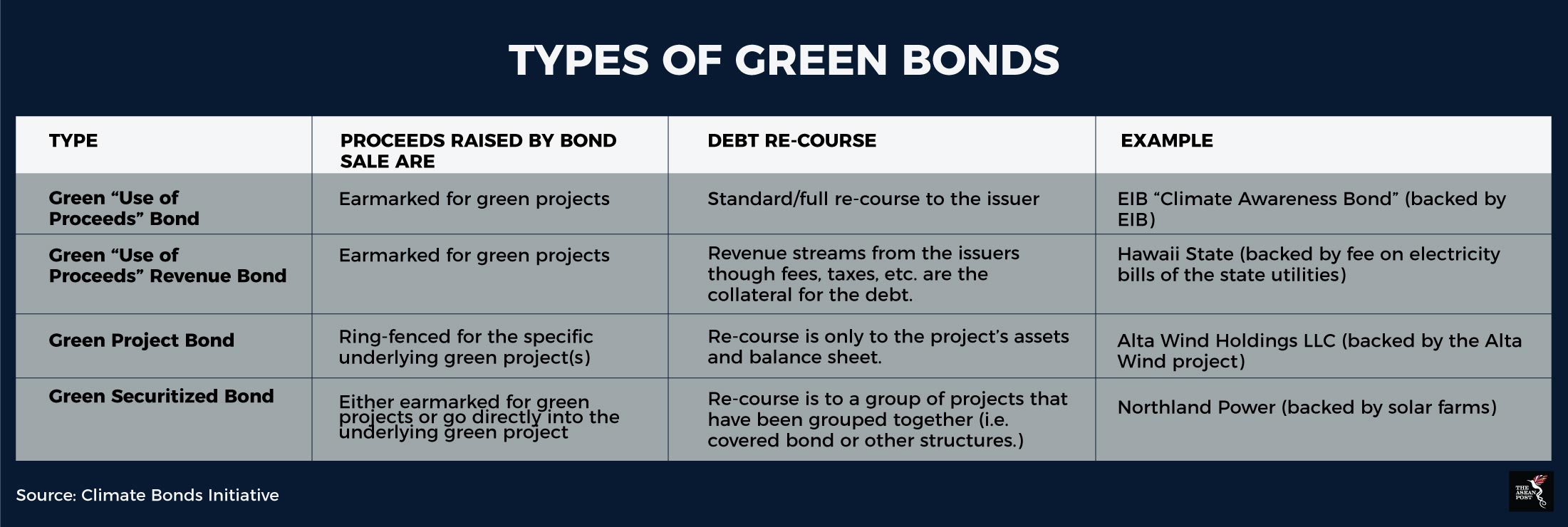

The basics of a green bond remain the same as any other regular bond. A bond is in effect, a promise between its issuer and the investor. The investor in purchasing the bond, lends that sum of money to the issuer. The investor should be paid back the full amount at the end of the bond maturity date, with interest payments being made at particular intervals during the tenure of the bond.

The difference with a green bond is that the money raised is used to finance businesses or projects that are “green” – have positive environmental and/or climate benefits. For example, in order for a project to be eligible for Asian Development Bank (ADB) Green Bond financing, it should fall under the following areas: clean energy; sustainable transport and urban development; green land use and forest management; building climate resilience; strengthening climate change adaption and mitigation policies, governance, and institutions.

Green bonds are especially attractive to investors looking to invest responsibly and feel the need to do their part in combatting the growing effects of climate change and other environmental challenges. It is also a way for companies to finance projects which might otherwise be difficult to finance via other, more traditional investment products.

Market opportunities for green investments

According to a 2017 report by Singaporean financial services group, DBS and the United Nations, member states of the Association of Southeast Asian Nations (ASEAN) require a fourfold year-on-year increase in green investment to protect their people and economies from the effects of climate change.

The report also stated that ASEAN green investment demand between 2016 and 2030 stands at an estimated US$3 trillion. The investments spread across various areas: infrastructure (US$1.8 trillion), renewable energy (US$400 billion), energy efficiency (US$400 billion) and food, agriculture and land use (US$400 billion). This also means that the market for ASEAN green investment is 37 times larger than the global green bond market was in 2016.

The report also stated that investment opportunities are plentiful as current annual ASEAN inflow of green finance is at an estimated US$40 billion only against an average need of US$200 billion a year from now to 2030. This leaves a gap of US$160 billion annually on average in financing that needs to be met. Indonesia will be requiring the largest volume of financing. Besides that, opportunities also exist in countries like Thailand and Vietnam.

ASEAN Green Bond Standards (AGBS)

The ASEAN Green Bond Standards (AGBS) was developed by the ASEAN Capital Markets Forum (ACMF) and launched in November 2017. The AGBS is intended to provide more specific guidelines than the international gold standard for green bonds, the Green Bonds Principle (GBP).

Its aim is to improve transparency, consistency and uniformity of ASEAN Green Bonds. It will also help develop a new asset class, reduce costs associated to due diligence and aid investors while making informed investment decisions.

The AGBS was first adopted by Malaysian investment institution, PNB Merdeka Ventures (PNBMV) to fund its Merdeka PNB118 skyscraper project. It will raise a 15-year tenure secured green sukuk (the Islamic equivalent of a Western bond) via an unrated Sukuk Programme of up to US$510 million, known as Merdeka ASEAN Green SRI Sukuk Programme.

“The ASEAN green sukuk validates PNB’s commitment to develop Warisan Merdeka as a sustainable and environmentally-friendly project,” said Abdul Aziz Mahmud, CEO of PNBMV.

“The Warisan Merdeka development has taken steps to ensure sustainable policies and best practices are in place for the building construction and operations, which are aligned with global standards. Upon completion, Merdeka PNB118 will be the first building in Malaysia that will satisfy the triple green building platinum accreditations locally and internationally, namely the Green Building Index (GBI), the Green Real Estate (GreenRE), and the Leadership in Energy and Environmental Design (LEED),” he added.

As it stands, green bonds are still a relatively new investment instrument in the region but as demand for greener investments increase, we could see a mushrooming of green bond issuances in the future.