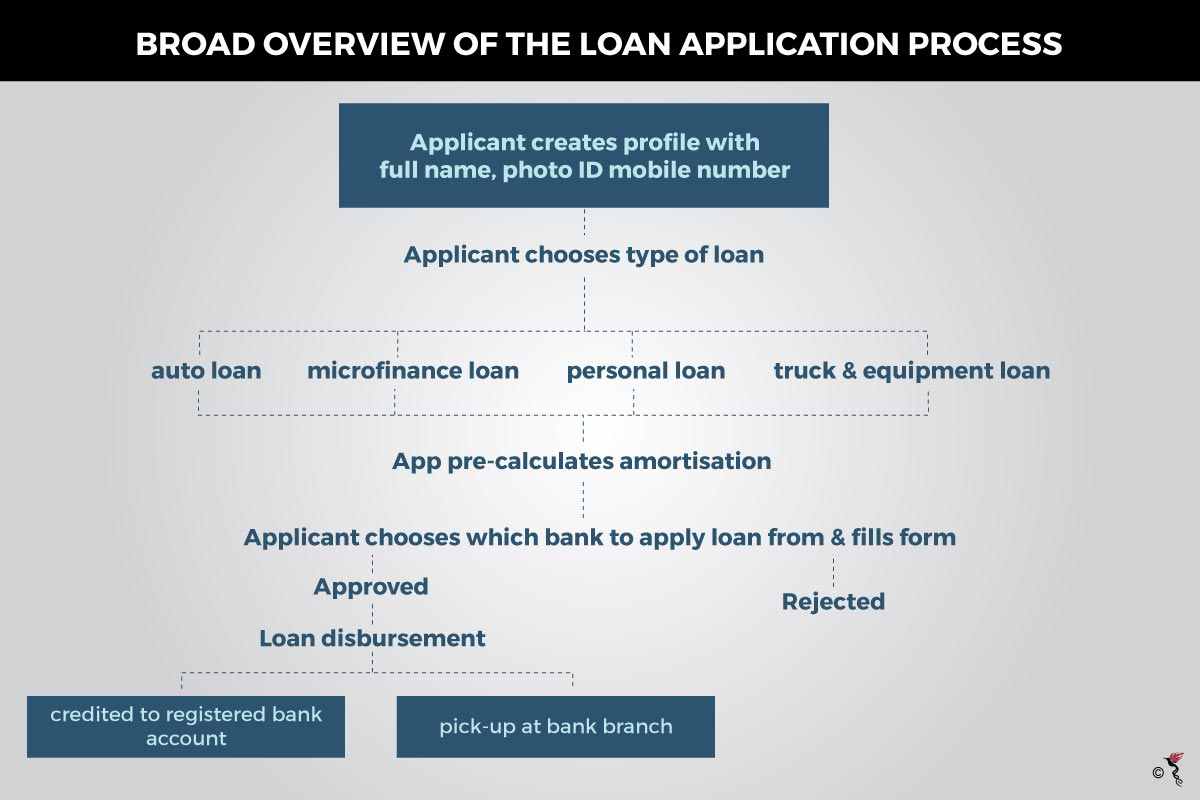

Technology has infiltrated most areas of our lives, so much so that we now take it with us everywhere.

Thus, even though creditworthiness has always been the domain of banks and other financial institutions, we now have digital lending apps to do the job for us, on-the-go.

In the Philippines, digital lending platforms like pera247, Moola Lending and Lendr are some of the apps and platforms that have gained a foothold in the lending business; offering small loans to a market mainly consisting of millennials, small entrepreneurs and SMEs.

These apps work by using various data points to mine data from a smartphone, including data usage, phone call duration, GPS location as well as time stamps to create a profile that shows user patterns. A smartphone payment account can also be used to trace financial data since expenditure is also recorded.

Compared to traditional credit agencies, the use of digital lending apps is far less daunting to operate as well a far more mobile, allowing people to access loans from anywhere and everywhere so long as they have a smartphone and internet connection.

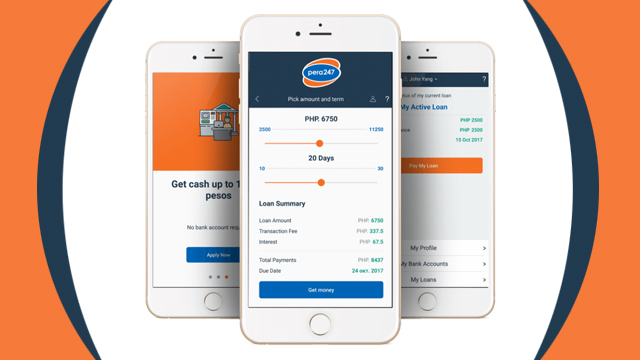

pera247, which touts itself as a provider of the fastest credit decision, uses algorithms that contain highly predictive digital credit assessment tech, with which it assesses smartphone data for credit scoring purposes.

The value of such data in making credit assessments has long been in debate, with the possibility of social media data also being considered.

A 2017 study conducted by economist Daniel Bjorkegren, for instance, shows how frequency of behaviour identified from smartphone data can be used as an indicator of an applicant’s ability to repay a loan.

The larger the digital footprint, the larger the data base from which data profiles can be created and put to work. This falls in line with how smartphone usage in the Philippines is expected to grow to 44.4 million by 2021 from its current 30.4 million, according to data from statista.com.

These platforms will then partner with lender institutions to provide the loans in question. FINTQ’s Lendr, for instance, currently partners with about 70 financial institutions, which includes the Landbank of the Philippines, Philippine Bank of Communications and Maybank Philippines.

“Borrowers who use Lendr are those with profiles that are targeted by banks. This only goes to show that our platform is really beneficial for our bank and non-bank partners as we work together in providing the financial needs of consumers,” managing director of FINTQ, Lito Villanueva said.

Lendr also reported that loans totalling PHP12 billion had been disbursed in 2017, bringing its total loans disbursement to PHP27 billion since its inception in 2015.

Whilst banks typically are unwilling to take on lower-tier customers because of the low pay-off, Lendr bridges the gap by obtaining such customers at a lower cost and then partnering with bank and non-bank lenders to provide those loans. This enables them to offer anything from medical and auto loans to SME loans; in essence providing banks with larger market share.

A screenshot image of the pera247 smartphone app.

The use of platforms like Lendr and pera247 are also appealing to lower-tier customers who may have no prior relationships with traditional banking institutions and may not have the confidence to repay bigger loans.

This includes SMEs, only 39% of whom cited banks as a source of funding in 2015, according to a Deloitte-Visa report. Overall, SME loan volume from banks was reported to be at only US$9 million, compared to Thailand’s US$171 million in 2014.

Access to bank-based financing was limited because of lack of credit information leading to slow allocation of funds as well as lack of proper guidance on how to apply for loans. Instead, SMEs had to seek financing from alternative sources, such as supplier credit, grants and capital leasing.

Though at present, potential lender institutions looking to partner with digital lending platforms could be concerned about the security risk of giving out such loans, ultimately, the payback could be lucrative when the SMEs produce fruit and contribute to the overall growth of the economy. In other words, traditional lenders should look at the potential of digital lending apps as part of their long-term strategy.

As digital lending continues to grow in the Philippines too, perhaps now would be the time to build a stronger regulatory framework that will address both financial risk management and data security, amongst other aspects. Greater financial education would also be necessary in order to reduce incidences of loan defaults, particularly among the yet unbanked.

Recommended stories: