Microfinance is described by the Financial Times Lexicon as a service where financial institutions will back small start-ups and would-be entrepreneurs with small loans, in the poorest parts of the world. In Southeast Asia, the biggest microfinance players currently include Asia Pacific-based LenddoEFL, Singapore's CredoLab and the Philippines’ Lendr, for example.

To add to this mix, Singapore-based ride-hailing service Grab will now join the fray. It recently announced plans to form a joint venture with Japan’s Credit Saison Co. to provide loans to consumers, micro-entrepreneurs and small-time entrepreneurs across Southeast Asia. The new joint venture will be known as Grab Financial Services Asia (GFSA) and will initially provide working capital loans and consumer goods financing to its existing pool of drivers, agents and merchants, among other things.

“Many in our region have no access to loans that they can use to purchase a new home or grow their small business. GFSA is building a reliable alternative to traditional credit scoring methods that is customised for the unbanked majority of consumers and small businesses in Southeast Asia, which will create economic opportunity for millions across the region,” Jason Thompson, managing director of Grab Financial told The Business Times in March this year.

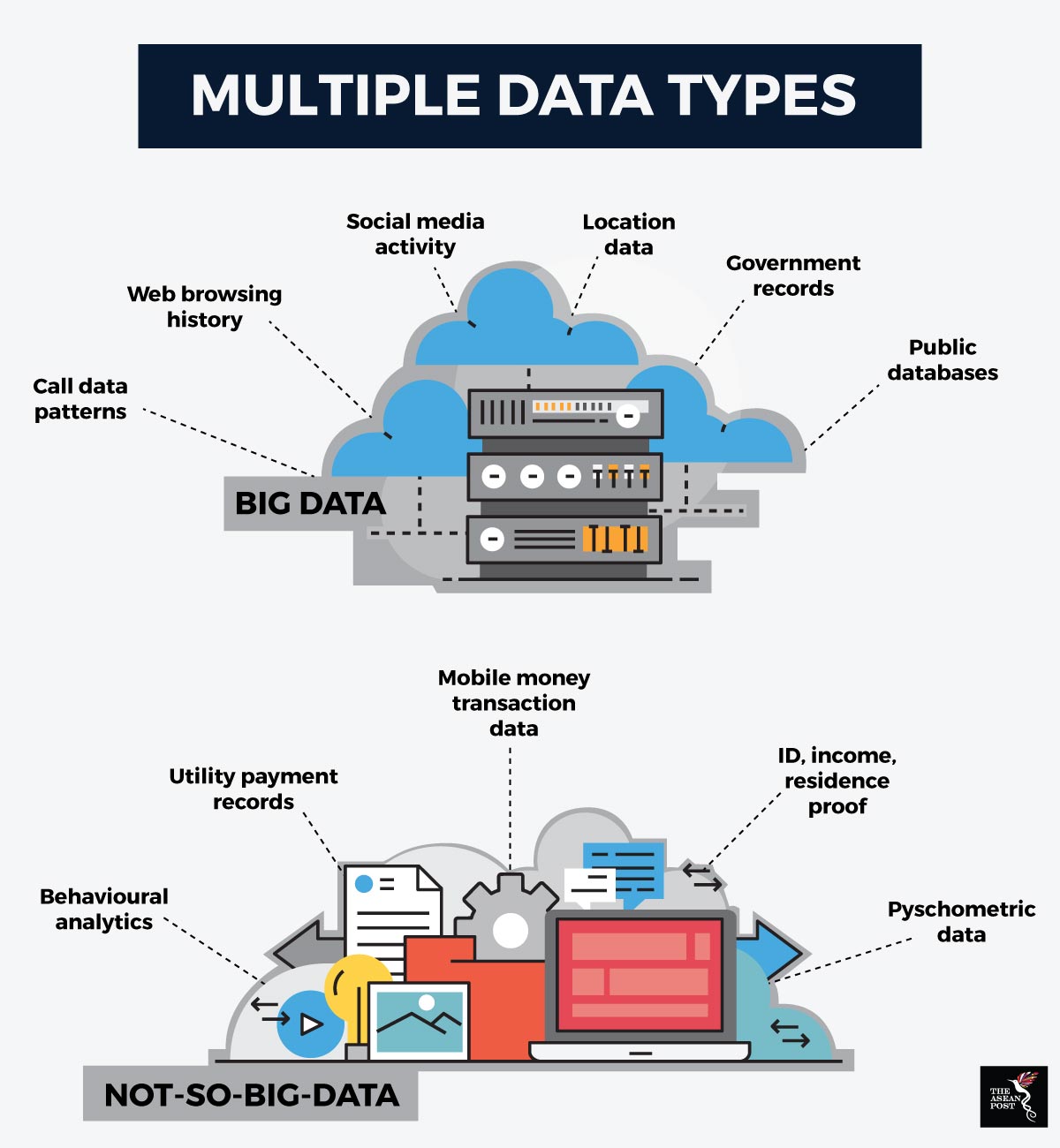

In this business model, big data, is used to assess a customer’s creditworthiness. Big data is defined as large volumes of structured and unstructured consumer data that can be gathered from a user’s entire profile of online activity, be it on social media platforms, product purchases or electronic check-ins. Such data is usually collected from various data points, which varies according to the type of online activity performed. An example of this is phone usage data which includes call duration as well as frequency of calls.

In microfinancing, it is this kind of data which will then be use to assess a customer’s ability to repay a loan. What is used is not the direct content of the data, but rather the behavioural patterns associated with the data collected. LenddoEFL, for instance, uses smartphone data, email and banking transaction data to assess the creditworthiness of a potential customer. A higher level of predictability in a customer’s behaviour, based on data collected, points to an increased likelihood to repay a loan.

Source: The Edge Markets Malaysia

Even so, the key is the use of big data to augment traditional bank data models, rather than to undermine their purview completely. A combination of the two types of data provides a clearer credit profile for microfinanciers to work with.

Microfinancing in Southeast Asia is still largely nascent, although there is plenty of potential for it to grow, due to the high levels of smartphone penetration here. This provides technology companies with large volumes of transaction data that they can funnel into alternative lending platforms.

Grab is one such technology company whose rapid expansion has been based on effective data leverage. So far it has used customer data to tailor its ride hailing and food delivery offerings to suit local needs in the eight Southeast Asian markets it currently operates in. The firm now has more than 86 million users across all of these markets. Launching microfinancing services is the natural next step after the launch of GrabPay back in November 2017, Thompson told the Singapore online publication, Today.

GrabPay refers to an e-wallet offering which was mainly aimed at Singapore’s neighbourhood hawkers, and small businesses.

Grab's rapid expansion into various market segments demonstrates the potential of big data to reach many different customer pain points, which can then guide it to create new products and services. Focusing on five key areas of data science, including markets, machine learning, optimisation, simulation and architecture has now allowed Grab to reach these niche markets more effectively.

Further technological developments in microfinancing may still be forthcoming, but much also depends on what the data is telling technology companies about the future. The future, as they say, lies in the potential of big data.