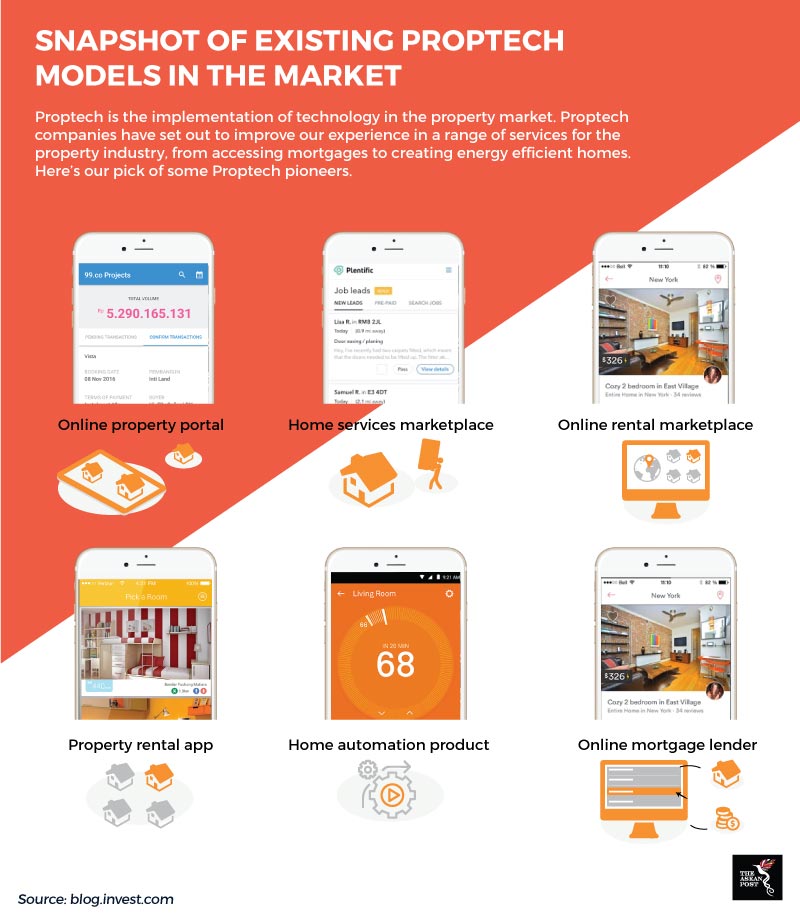

According to Anthony Couse, Asia Pacific CEO of real estate and investment management firm, Jones Lane LaSalle (JLL), proptech refers to the utilisation of technology to create or renovate services offered in real estate to buy, sell, rent, develop, market, and manage property in a more efficient and effective way.

Broadly speaking, proptech is delivered across three main mediums, namely hardware, software and blockchain, according to Desmond Sim, head of CBRE Research in Singapore and Southeast Asia. The current wave of proptech builds upon the first wave which began in the mid-1980s, and which consisted mainly of the use of portals to consolidate property market listings and property agent information, among other things.

These days, proptech will more likely build on the innovations offered by blockchain, cryptocurrencies, virtual reality and the internet of things; all of which could either be disruptors or enablers, depending on the conditions of the local real estate market.

The transparency offered by blockchain technology could create new structures of home ownership, for example.

“We want to create a new model where the community as a group would be actually able to own properties and will be able to share the utilisation of these properties among themselves,” noted Darvin Kurniawan, CEO of blockchain startup, REIDAO.

Proptech startups across the Asia Pacific region gained US$4.8 billion in investments between 2013 and 2017, according to the ‘Clicks & Mortar: The Growing Influence of Proptech’ report commissioned by JLL. In Southeast Asia, this growth has been more sporadic, because there is less overall awareness of how proptech can be integrated into existing property offerings.

Proptech in Singapore is in a more advanced stage as it builds on the Singapore government’s Smart Nation initiative. The government there launched its Real Estate Industry Transformation Map on 8 February, 2018 in a bid to leverage technology for innovation and to drive professionalism and skills in the workforce. A workgroup was further launched in relation to this initiative to focus on a number of areas, including establishing digitalised contract templates and checklists by the early 2020s. The move is in part a response to the consolidation of Singapore’s real estate sector, including a number of mergers and acquisitions between the state’s largest property brokerages in 2017.

The prospects for proptech in Malaysia are also promising, although the scene there is still budding. According to reporting by The Edge Markets this year, Malaysia’s IFCA will soon launch an accelerator program in partnership with Google Cloud in a bid to nurture local proptech startup firms. The accelerator program will help them gain access to mentorships, funds and networking opportunities. However, there needs to be similar technological adoptions by the wider property ecosystem encompassing architects, engineers and construction firms.

One of the agreed conclusions among industry players at the MIPPM Property Management Conference in 2017, was that joint management bodies and management corporations in Malaysia are overall still cost-conscious in their approach towards technology adoption.

It is also arguable that wider technological adoption is needed across sectors, such as the possible availability of technology to vet and facilitate property transactions. Whether proptech is something that will potentially eliminate the human factor is also another point for regulatory authorities to consider. It is worth arguing that property-related transactions usually involve large-enough sums of money and require some form of trust in the vendor, something which only interpersonal relationships can effectively foster.

While new technologies can offer some hope for property markets in Southeast Asia, it is still not likely to transform the wider industry, as market forces will still be at play. At present, Southeast Asian countries still need to lower the financial barriers linked to homeownership, something which governments and banks need to play a part in. Affordability measures such as policies to supply more public housing in Myanmar and loan assistance for home purchases above the value of US$10,000 in Thailand, for instance, need to be in place before proptech can effectively ride on any purchasing wave that could follow.

Proptech is not likely to be a disruptor in Southeast Asia anytime soon, but it could be an enabler in tandem with growing developments in Southeast Asia’s property markets as they mature. This, in turn, is only likely to come about with the progress of time.