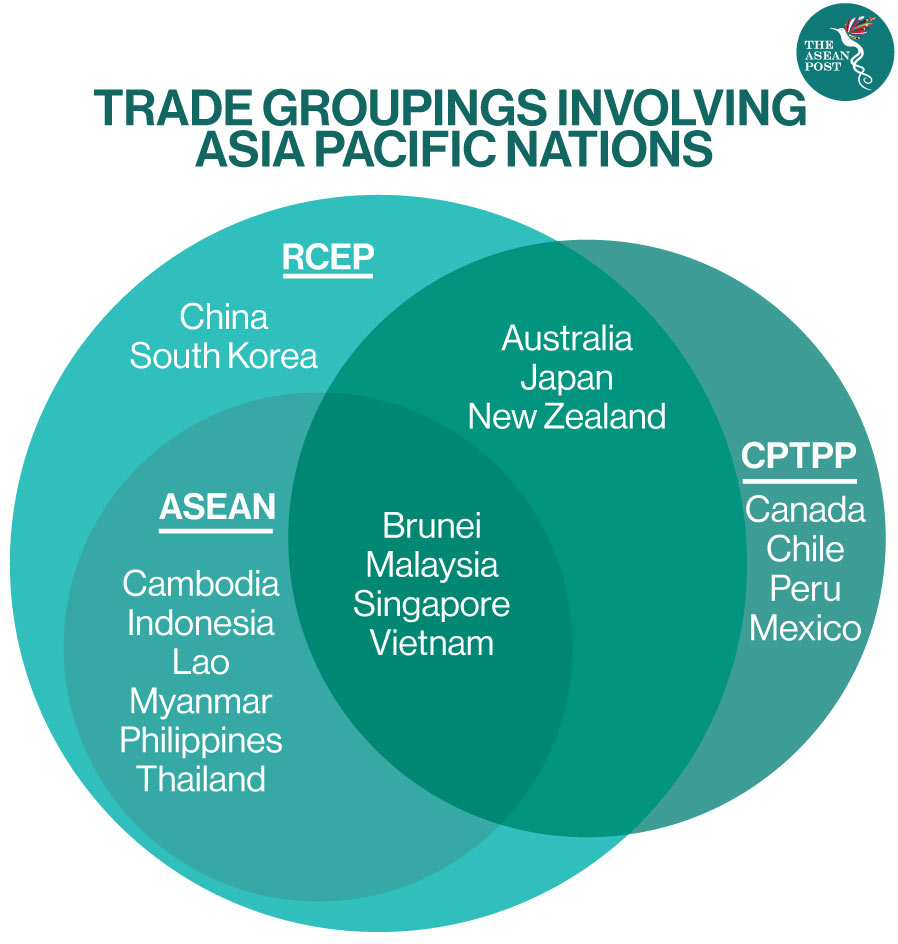

With the signing of the Regional Comprehensive Economic Partnership (RCEP) on 15 November, the stage is set for Malaysia to tap into the world’s largest free trade area (FTA) with 2.1 billion consumers, including China, and accounting for approximately 30 percent of the world’s gross domestic product (GDP).

Up next is the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) – spanning the Asia-Pacific Rim countries and home to 95 million consumers as well as contributing around 13.5 percent of global GDP worth a total of USD10.6 trillion.

The CPTPP is a gargantuan FTA in terms of the scope of provisions running into thousands of pages. Previously, it was known as the Trans-Pacific Partnership (TPP) under the lead sponsorship of the United States (US). Essentially, the TPP was perceived to be biased in favour of the rights and interests of multinational corporations, i.e. foreign investors (based in the US), over governments as sovereign entities. Both, the TPP and CPTPP exclude China.

Fair Not Just Free Trade

Even with the withdrawal of the US from the TPP, the CPTPP or the new version of the TPP remains highly controversial. It’s good that Minister of International Trade & Industry Azmin Ali has reiterated Malaysia’s stand that there’s no timeline to ratify the CPTPP. And that ratification must be dependent on the CPTPP being about “fair” trade and, therefore, not just about “free” trade.

Such caution is to be welcomed because both, the old TPP and new CPTPP are not a standard FTA and that the basic provisions of the TPP remains intact in the CPTPP.

Well-rehearsed arguments opposing the TPP include: (a) the prospects of imported products threatening to swamp the local market and thus, threatening to put domestic producers and suppliers out of business as well as inflationary pressures; and (b) the fear that the Bumiputera (ethnic Malay) agenda and government procurement policy in relation to Bumiputera contractors as well as local small and medium-sized enterprises (SMEs) will be undermined in the name of “convergence”, “non-regression”, or “level playing field”.

Added to that is the issue of state aid, i.e. government or State intervention in the private sector targeted at nurturing and developing certain industries and sectors. Outside of Malaysia, South Korea with its chaebols and Japan with its zaibatsus are classic examples.

Under the CPTPP, state aid rules remain a major concern. As highlighted in a report by Khazanah Research Institute (KRI) – a research institute sponsored by Khazanah Nasional Berhad, Malaysia’s sovereign wealth fund – Chapter 17 of the CPTPP specifically mandates “level playing field” between state-owned enterprises/SOEs (government-linked companies/GLCs) at the federal level and non-SOEs (read: foreign investors). This would definitively impact the advantages enjoyed by Malaysian GLCs from the government (institutional, regulatory, financial).

In addition, the TPP was also opposed within Malaysia on grounds revolving around investor-state dispute settlement (ISDS) and intellectual property rights (IPR).

Firstly, on ISDS which basically means disputes between the government and foreign investors are to be arbitrated by a non-judicial tribunal outside of the country’s sovereign jurisdiction.

Given developments post-TPP which spill over into the current CPTPP context, the worry is that in the event the government of Malaysia chooses to cancel or renegotiate a contract with a foreign investor as was the case with the East Coast Rail Link (ECRL), just to give an example, will this expose the country to ISDS proceedings? This on the basis that it constitutes a form of “indirect expropriation” and breach of investment obligation?

Secondly, on intellectual property rights (IPR), there’s the well-acknowledged and well-founded argument that the TPP would have resulted in the prices of drugs soaring, thus impacting access for those with a low income, due to patents enforcement and licensing requirements.

Now under the CPTPP, the suspension of longer patent periods for innovative medicines and shorter periods for copyright protection may be welcomed as good news for Malaysia. But will the inbuilt bias against data localisation work to the adverse disadvantage of new entrants into the CPTPP market, not least of all from Malaysia?

Data localisation means data collected must be first approved by the host country before being transmitted across borders. Prohibiting data localisation benefits countries with strong patents applications and track record. New data from one country can be used as part of the subsequent newer patent submissions in another country, with all the ramifications on the host country including loss of tax revenue due to ease of transfer pricing, for example.

Ironically, this undermines a level playing field.

Thirdly, on electronic commerce. Will Malaysia’s accession to the CPTPP render the digital service tax (DST) under the Service Tax Act (2018) susceptible to legal challenge as being incompatible with the provisions on electronic commerce as per Chapter 14 of the CPTPP?

The relevant provisions mention the prohibition of the “imposition of customs duties on electronic transmissions”. Will the DST be interpreted under the ISDS as constituting a violation of the government’s “investment obligation”, where the digital content providers that are the foreign service providers (FSPs) have operations in Malaysia, whether outsourced or through subsidiaries?

Intra-ASEAN Cooperation

Furthermore, will the DST be deemed as a form of customs duty and, therefore, a form of protectionism? Bearing in mind, legal action can still be initiated by an interested party based in Malaysia with legal standing on the basis of judicial review. Thus, the relevant stakeholders who may be aggrieved needn’t go through the ISDS which of course has a much higher threshold, for example, requiring demonstration of loss of investments.

Last but not least, as we pause to consider ratification of the CPTPP, have we weighed the potential impact on intra-ASEAN cooperation and regionalisation? Will the CPTPP also simultaneously weaken ASEAN’s “centrality” as the “fulcrum” of wider Asia-Pacific cooperation – which lies at the core of the RCEP?

The government of Malaysia is right to be focussing and being committed towards accelerating and intensifying intra-ASEAN cooperation and coordination by prioritising the RCEP. In doing so, we’re tapping into the vast potential of ASEAN and the wider RCEP market that’s also more supply-chain resilient while at the same time taking advantage and playing a part in shaping the reshoring and onshoring phenomenon of the supply chain reconfiguration.

Related Articles:

Huge Asian Trade Pact Signed In Coup For China

How The CPTPP Could Widen Inequality