20 years ago, no one could have accurately predicted the huge impact that inventions like the smartphone and the World Wide Web would have on humankind. As technology advances at a breakneck pace, the same could be said about blockchain technology.

It’s a common misconception to conflate blockchain with cryptocurrencies like Bitcoin, Ethereum and Litecoin. While the technology gained prominence because it served as the basis of today’s cryptocurrencies, the technology itself has a myriad of uses outside that function.

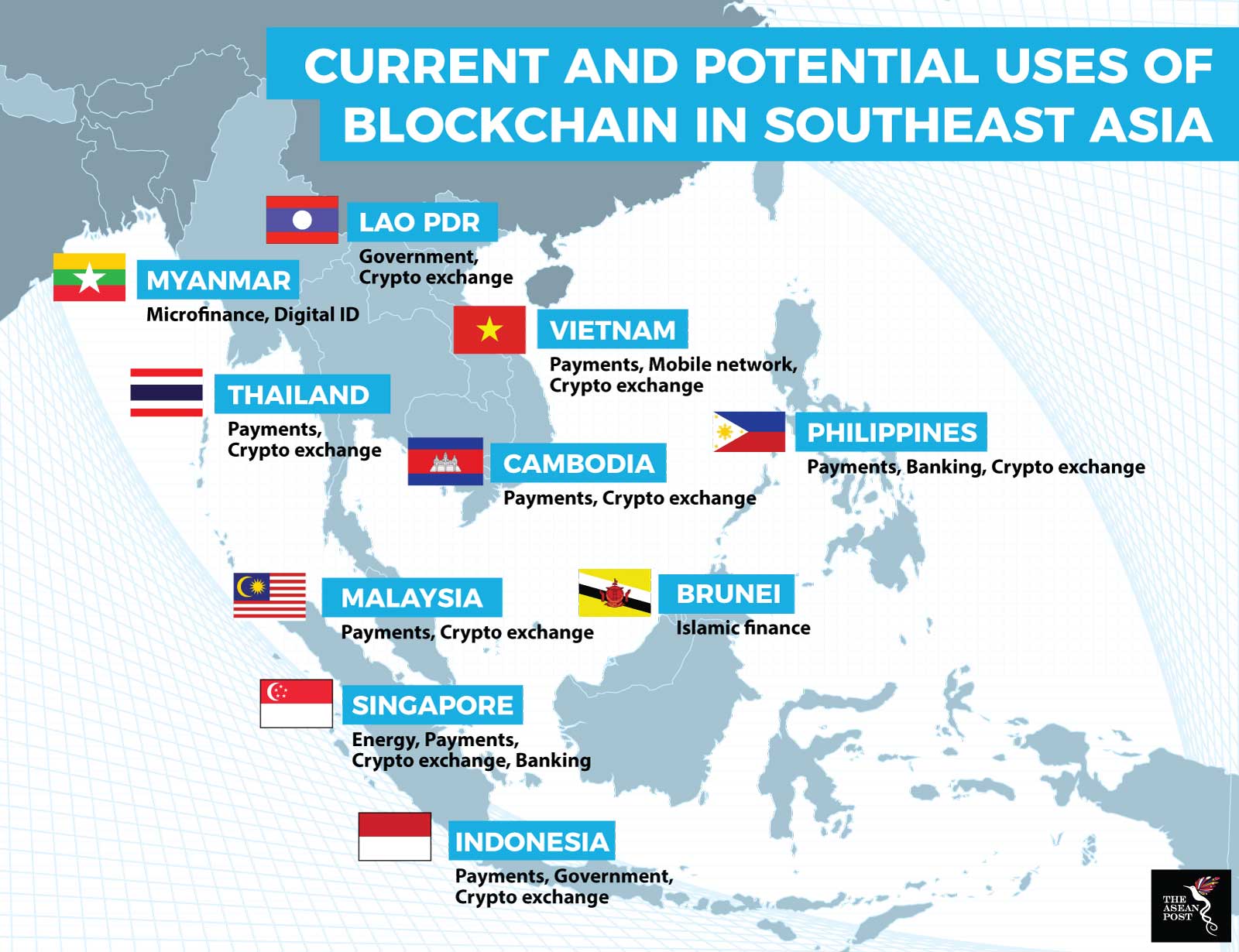

Blockchain has been touted to revolutionise global supply chains, 21st century industries and even governance. Its versatility and decentralised nature have gained significant currency in Southeast Asia and many governments within the region have warmed up to the prospect of promoting the integration of this technology into businesses and the public sector.

Leading the curve

Thailand has been most eager to adopt blockchain technology in the region. The country has already enacted laws that govern cryptocurrencies and is planning for a blockchain token for instant securities settlements. Recently, its central bank revealed that it is considering blockchain applications for cross-border payments, supply chain financing, and document authentication.

According to the Governor of the Bank of Thailand, Veerathai Santiprabhob, the use of technologies like blockchain “can help safeguard financial information and reduce the number and magnitude of fraudulent activities.”

Singapore has by far been the most receptive towards blockchain technology especially when it concerns Initial Coin Offerings (ICO). The island nation has become a top destination for ICOs, especially for Chinese companies after China banned ICOs, calling it an illegal fundraising tool. Singapore’s government and private sector have set up incubators and investment funds focussing on cryptocurrencies and other uses of blockchain.

Besides that, the island state has also begun experimenting on a ground-breaking use of blockchain technology in the energy sector. Singapore-based Electrify uses the technology to create a peer-to-peer energy market where electricity can be bought and sold at cheaper rates. The start-up recently raised US$30 million in funding and is looking to penetrate the Singaporean market further when regulations which allow users to select their preferred energy provider come into effect.

Across the causeway, Malaysia houses the New Economy Movement (NEM) Foundation blockchain centre – the largest of its kind in Asia. It will serve to educate the masses on the technology as well as accommodate burgeoning blockchain based start-ups via incubator and accelerator programs.

Source: Various sources

Malaysia’s central bank has been receptive towards the use of such technology within the banking sector. Among others, it has a fintech sandbox which allows fintech companies – even those without a presence in Malaysia – to participate in it for a testing period of not more than 12 months. On top of that, it is taking necessary steps to police and regulate cryptocurrency use within its borders. In a published report, nine cryptocurrency regulators have been registered with the central bank.

Promising progress

Indonesia’s blockchain sector is eager to take advantage of the opportunities present. Over the past year or so, it has seen an explosion of blockchain related start-ups – initially focussed on cryptocurrency that are now venturing into other areas.

Moving forward, blockchain could potentially revolutionise government, supply chain logistics, consumer transactions and data security in the country. Both the public and private sectors are looking to collaborate to overcome challenges linked to data management. For example, blockchain-driven application Online Pajak helps improve transparency as well as reduce the paperwork burden related to the tax system.

In Vietnam, a fertile start-up ecosystem will likely pave the way for the development of blockchain applications. The government there recently kickstarted preparations for a fintech sandbox which could be utilised by blockchain-related start-ups. Companies like mobile network provider Viettel and intermediary payment services provider, Napas have been experimenting with the technology and have rolled out several pilot projects.

The Philippines has also recognised blockchain as a revolutionary tool and with the inception of the Blockchain Association of the Philippines (BAP) in May this year, more information and guidance would be readily available for anyone interested in using this technology. Led by Justo Ortiz, chairman of the Union Bank – one of the largest banks in the archipelagic nation – BAP hopes to help small and medium enterprises deploy the technology in order to provide them with a competitive edge.

Moreover, in a bid to improve financial inclusion in the state, Union Bank has also picked five rural banks in Mindanao – the second largest island in the Philippines – for a blockchain pilot program that will test real-time, cheaper retail payments. The initiative is set to link rural banks to the country’s main financial network.

Elsewhere, blockchain technology is still in the early stages of integration in Lao PDR, Brunei, Cambodia and Myanmar. Its uses range from providing financial services to e-government initiatives. While nothing palpable has come out of it as yet, such initiatives demonstrate an increasing awareness of blockchain as a fundamental technology for the future.

Related articles:

A blockchain boost for the airline industry

Singapore’s Project Ubin enters next phase