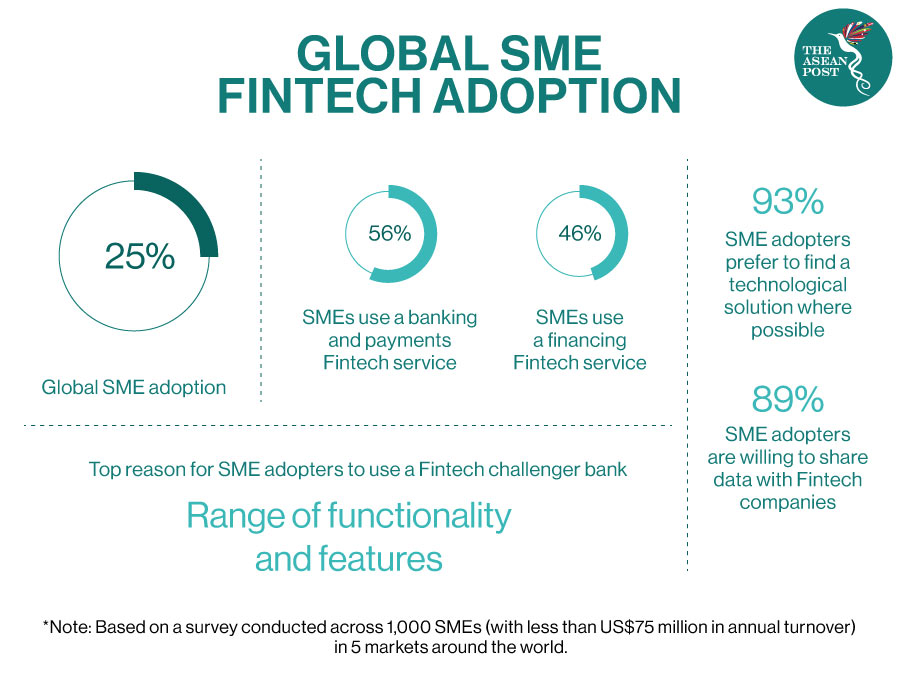

Financial technology or fintech is not only the new kid on the block, but a pivotal game-changer for the digitalisation of small and medium-sized enterprises (SMEs).

Quoting from professional services network firm PricewaterhouseCoopers (PwC), fintech is simply the evolving dynamic intersection and strategic overlap between financial services and technology.

Presently, SMEs are having to grapple with cash flow problems – with growing unsettled and accumulating liabilities in their balance sheet while expecting to shoulder much of the burden to remain afloat. This includes employment retention as well as settling their tax and other liabilities, among others, in the form of operating and overhead costs.

Ernst and Young (E&Y) in its Global FinTech Adoption Index 2019 reported that the adoption rate of fintech have been exponential, leaping from 16 percent in 2015 to 64 percent in 2019. This global trend portends and augurs well for the potential and future digitalisation of Malaysia’s economy.

Therefore, the phenomenal growth of fintech can serve to catalyse the digitalisation of Malaysia’s SMEs.

As such, even as calls for SMEs to digitalise picks up momentum, the increasing role of fintech should also correspondingly be brought to the forefront.

Hence, fintech – although not quite the missing link – in the evolving landscape SMEs are operating in, particularly given the impact of COVID-19, is the one indispensable component. That is, in the reconfiguration of the way businesses that have yet to digitalise survive and thrive.

According to the Fintech Malaysia Report 2019 by Fintech News, there are 198 players offering fintech services.

In its Fintech and Digital Banking 2025 Asia Pacific, market research company IDC reported that financial liberalisation, drive towards cost-reduction and savings, intense competition from counterparts as well as P2P (peer-to-peer) players, and wafer-thin net interest margins, among others, are pushing banks to further automate, through robotic process automation (RPA) software that enables computers to process the manual workload of the business more efficiently and effectively (e.g. by triggering error-free responses).

Still, despite the growth of the fintech industry in Malaysia, many small businesses are still reliant on traditional sources of borrowing – savings, loans from relatives and friends, and non-bank money lenders such as pawnbrokers.

This persistent trend is in tandem with the current challenge of digitalising SMEs as a whole, where despite the various initiatives undertaken by the government, the momentum has not been as forthcoming.

According to a white paper by SMECorp and Huawei Technologies titled, “Accelerating Malaysian Digital SMEs: Escaping the Computerisation Trap” (2018), only 44 percent of SMEs are using cloud computing. Most have not adopted cloud software-as-a-service to drive software process improvements. Instead, cloud storage services such as Dropbox are a common feature.

This means that in the context of the post-COVID-19 era, we are starting at a baseline that requires greater synergy between the government and SMEs – to achieve the desired outcome of full-scale digitalisation.

Promoting fintech as a key driver of SMEs would entail the following two strategic thrusts: (1) The government playing an indirect role of incentivising and pushing SMEs to take advantage of fintech financing opportunities; and (2) The government directly enabling SMEs to move up the digitalisation chain/ladder.

Fintech Via P2P And ECF

Fintech is poised to overtake conventional banking and finance as well as non-banking sources as the leading source of financing opportunities for SMEs. External factors like COVID-19 alongside government inducement will lead to increasing pressure (direct and indirect) on SMEs to adapt or be left out and ossify.

Funding Societies Malaysia and B2BFinPal are the two leading domestic or local players in the market currently in terms of P2P and Equity Crowdfunding (ECF) also known as co-investment.

The Securities Commission (SC) has also been working with the government to launch the Malaysia Co-Investment Fund (MYCIF) of RM50 million (US$12.3 million) targeted at capital markets, including companies listed on the Leading Entrepreneur Accelerator Platform (LEAP) Market board (for SMEs).

Since 2019, the SC has lifted the funding limit on ECF platforms to RM10 million (US$2.4 million), and allowed ECF and P2P platforms to operationalise secondary trading with immediate effect.

From 21 ECF and P2P platforms registered with the SC that have collectively raised RM587 million (US$144.4 million) for more than 1,600 micro, small and medium enterprises (MSMEs), fintech platforms have now helped more than 2,500 SMEs to raise over RM1 billion (US$246.1 million), according to the latest figures by the SC.

Simultaneously, fintech will play a critical role in reducing red-tape in the processing of credit/loan applications. Technology, particularly the use of artificial intelligence (AI) and big data will be an integral and essential feature and dimension in how credit/loan applications are fast-tracked.

Government As Enabler

It is vital to ensure that the trend of increasing assimilation of fintech as a major source of funding keeps up with the trend of increasing digitalisation and vice-versa.

Fintech is simply a subset of digitalisation. Digitalisation of SMEs’ operational capacities should logically and organically extend to the adoption of fintech as the alternative channel of credit.

Fintech is not just a crucial source of funding and borrowing for SMEs in the long-run – as part of the alternative solution to ease cash flow problems – but is also an impetus and catalyst for the growth of digitalisation.

The ecosystems of both fintech and digitalisation, therefore, complement and supplement each other.

Moving forward, a closer strategic collaboration between the government and SMEs is needed.

In this, the Malaysian Digital Economy Corporation (MDEC) has been at the forefront in promoting and augmenting fintech and driving the digitalisation of SMEs. In August this year, MDEC – in collaboration with the Central Bank of Malaysia (Bank Negara Malaysia) – launched the “Fintech Booster”. It provides capacity building programmes for fintech companies – which are themselves SMEs – based in Malaysia to develop meaningful, innovative products and services by enhancing their understanding of market, compliance and regulation requirements.

Rais Hussin, Chairman of MDEC said that Malaysia “is in a strong position to harness various opportunities that Islamic fintech has to offer” which is still in its infancy in the country as only a handful of SMEs are utilising it.

Under Budget 2021, the government will continue to nurture the development of P2P lending and the ECF eco-system. A RM50 million (US$12.3 million) matching grant for P2P lending and RM30 million (US$7.3 million) matching grant for ECF have been allocated, respectively. Additionally, individual investors are entitled to a 50 percent income tax exemption with a limit of RM50,000, (US$12,306).

There is no doubt that the government of Malaysia is doing its best to help SMEs transition towards digitalisation – in line with the broader move up the value chain for the economy of the future. But SMEs on the whole, especially those that have yet to digitalise need to do their part.

Related Articles:

Digital Banking In Southeast Asia